Markets

- John M West III, MBA, CFP®

- Jan 20, 2023

- 2 min read

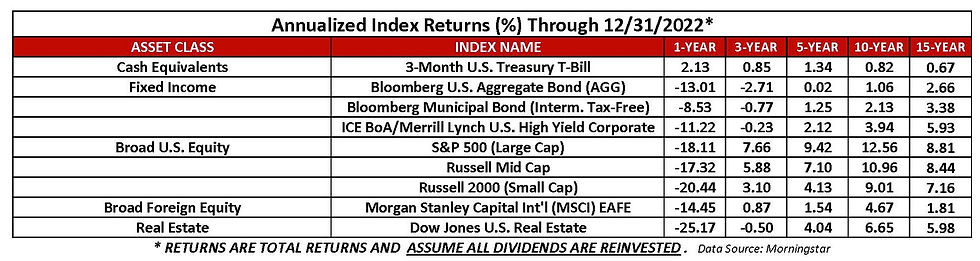

After a bull market that lasted nearly 15 years, markets experienced a massive pullback in which nearly every asset class was down. 2022 was one of only five years in the last 100 where both bonds and stocks finished in the red. The ONLY positive category for the year was cash, but even that was negative after adjusting for inflation. It was the worst selloff since 2008, primary due to the Federal Reserve's tightening policy to inhibit growth and bring down inflation.

Fixed Income: Tax-free bonds led for the quarter, while cash led for the past 1 and 3 years. High-yield corporate bonds led during all other time periods. Aggregate bonds were the laggard in all periods through 5 years, while cash was the worst performer over the past 10 and 15 years.

As the Fed nears the terminal rate, bonds provide tremendous value as bonds provide a much higher yield than they did a year ago. Moving forward, they should provide the ballast we have come to expect.

Equities: Foreign equity led for the 1-year, while large U.S. stocks led for all other time periods. Real estate was the worst performer over the 1 and 3 years, while foreign was the laggard in all other time periods.

The global economy is slowing down to combat inflation and patience will be crucial throughout 2023. ALWAYS remember that stock prices are a forward-looking projection of what is expected to happen, NOT what is currently happening in the economy. Getting inflation back under control will not be a quick fix. As a result, a recession is certainly possible and more likely than not to occur. However, over the long run, the markets come back stronger. New highs will be achieved again.

During the past 20 years in my career, the last 13 of which have been with Susan, I have observed that those disciplined investors who continue to buy through both up and down markets are far more likely to meet their long-term objectives. In the meantime, your allocation needs to match your goals based on the amount of risk necessary to meet your needs as we all embrace this exciting new chapter together.

Comments