Global equity markets started the quarter strong but saw declines in large-cap U.S. and foreign stocks throughout March as the conflict in Iran escalated. Even with the turmoil, mid-cap and small-cap U.S. stocks ended the quarter in positive territory, while bonds finished relatively flat.

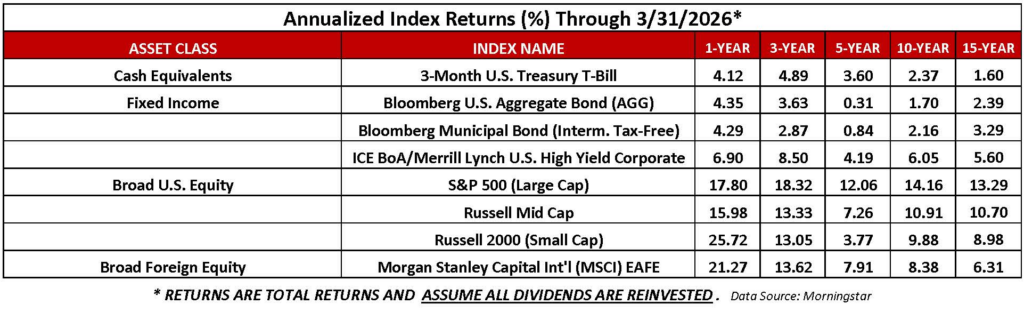

Cash & Fixed Income: Cash led for the quarter, while high-yield bonds led for all other periods. Cash was the laggard in the 1- and 15-year periods, while high-yield lagged in the quarter. Tax-free bonds still lag for the 3-year period, while aggregate bonds were the worst performer in the 5- and 10-year periods.

In January, we trimmed bonds and alternatives for required minimum distributions (RMDs). In March, we fully rebalanced portfolios, including bonds and alternatives for those clients who were underweight their targets. While the Iran conflict accelerated in the latter part of the quarter, bonds and alternatives provided the ballast in client portfolios when equity markets pulled back. With interest rates unchanged, bonds also continued to provide consistent income in the first quarter, along with our alternative funds, which all generated positive quarterly returns.

Equities: Mid-cap stocks led during the quarter, and small-cap stocks for the 1-year. While large-cap stocks still led in all other periods, they were the laggards in the quarter. Mid-cap lagged in the 1 year, and small-cap was the worst performer in the last 3 and 5 years. Foreign stocks still lag in the 10- and 15-year periods.

In January, in addition to trimming bonds and alternatives, we trimmed overweight equity for client RMDs and purchased money market funds for those clients who did not have an immediate cash need. In March, we added to underweight equities as part of a full portfolio rebalance.

Currently, global oil prices may remain elevated due to the restricted flow of oil tankers through the Strait of Hormuz. Geopolitical uncertainty supports having a globally diversified portfolio including equities, fixed income, and alternatives that align with your long-term risk tolerance. We will keep portfolios in line with long-term model allocations until there is more clarity in global markets. Our current portfolio positioning remains tilted towards higher-quality companies that should continue to generate positive cash flow. As always, we will continue to monitor the situation and adjust portfolio allocations when necessary, without overreacting to short-term market-moving events.

This Commentary is provided by Spraker West Wealth Management, a registered investment advisor, and is for informational purposes only. It should not be construed as investment advice and is not intended as a solicitation of any specific product or service. Investments and/or investment strategies include risk including the possible loss of principal. There is no assurance that any investment strategy will achieve its objectives. Information provided is not intended as tax or legal advice and should not be relied upon as such. You are encouraged to seek tax or legal advice from a qualified professional.